3 CD Strategies to Grow Your Savings Faster

Earn more money with CD rates.

Published Tuesday, February 4, 2025 to Advice

Have you ever heard the term “make your money work for you”? What does that even mean?

Simply put, it means investing in something that makes your money grow faster than it would in a standard savings account. Many people look to stocks, bonds, EFTs and more.

Those are all great investment options. With a little help from the experts, those investments can be quite lucrative.

But they also come with risks.

If you want a low-risk, steady-return investment option, look no further than a CD. Investing in a CD with a little strategy can help you balance growth and flexibility.

How Do CD Rates Work?

A certificate of deposit (CD) is as close to a sure thing as you can get as an investor. And they’re very simple: invest your money for a set amount of time and earn a steady profit with a fixed CD rate over the full term.

In most cases, CD rates are significantly higher than simple savings accounts. This makes them ideal for growing your money faster.

For example, the average savings account rate as of December 2024 is 0.60% APY, according to Bankrate. But the average rate on a 1-year CD is 1.68% APY.

| Account Type | Rate |

|---|---|

| Savings Accounts | 0.60% APY |

| 1-year CD | 1.68% APY |

| 3-year CD | 1.35% APY |

| 5-year CD | 1.34% APY |

| ^ According to Bankrate.com, December 2024 | |

However, you’ll want to ensure you don’t need those funds before your CD matures. This will help you avoid paying a penalty and potentially forfeiting interest earnings.

When You Should Get a CD

There are several factors that make a CD the right choice for you. Here are a few reasons you may want to open a CD:

- CD rates are higher than your savings account rate.

- You don’t anticipate needing to spend your money for a while.

- You want to earn more without the risk of the stock market.

3 CD Strategies to Maximize Your Savings

Balancing steady growth with flexibility requires a well-planned CD strategy. There are three primary strategies you can look to when investing in CDs:

- CD Ladder

- CD Barbell

- CD Target

The CD Ladder

A CD ladder is a strategy that includes splitting your investment between multiple CDs, each with a different maturity date. Then you’ll have CDs maturing periodically and you can choose whether to reinvest your money in another CD at that time.

For example, if you have $7,500 to invest, you could create a CD ladder by investing $2,500 in three CDs, with one maturing every three months.

- 9-month CD

- 12-month CD

- 15-month CD

As each of those matures, you can decide to withdraw your investment or reinvest it in a longer-term CD with a higher rate to maximize your earnings. If you do reinvest in long-term CDs, those will also mature every three months.

Learn More: CD Ladder Strategy

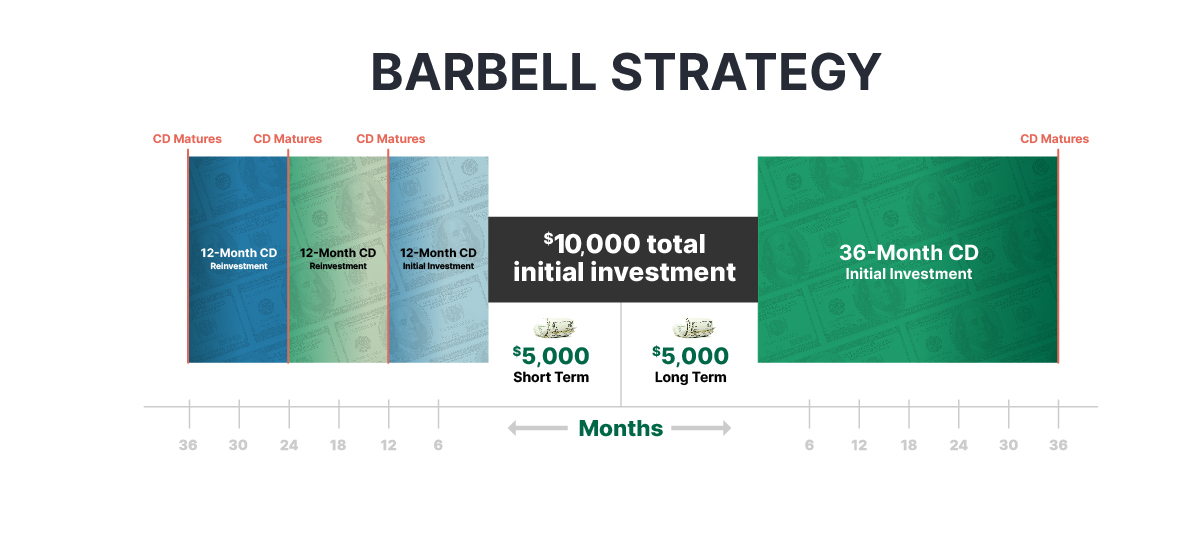

The CD Barbell

A CD barbell includes splitting your investment in two: one long-term CD and one short-term CD. If rates have gone up by the time the short-term CD matures, you can reinvest it in a long-term CD with the higher rate. Otherwise, you may keep the money or reinvest it in another short-term CD until rates do go up.

The key here is to balance long-term growth and high interest rates with short-term flexibility and access to your funds sooner.

This approach could also work if you have long-term and short-term goals. The short-term CD will mature much faster and you will have access to withdraw your money much sooner. Then the long-term CD can help you meet a different savings goal further down the road.

Learn More: CD Barbell Strategy

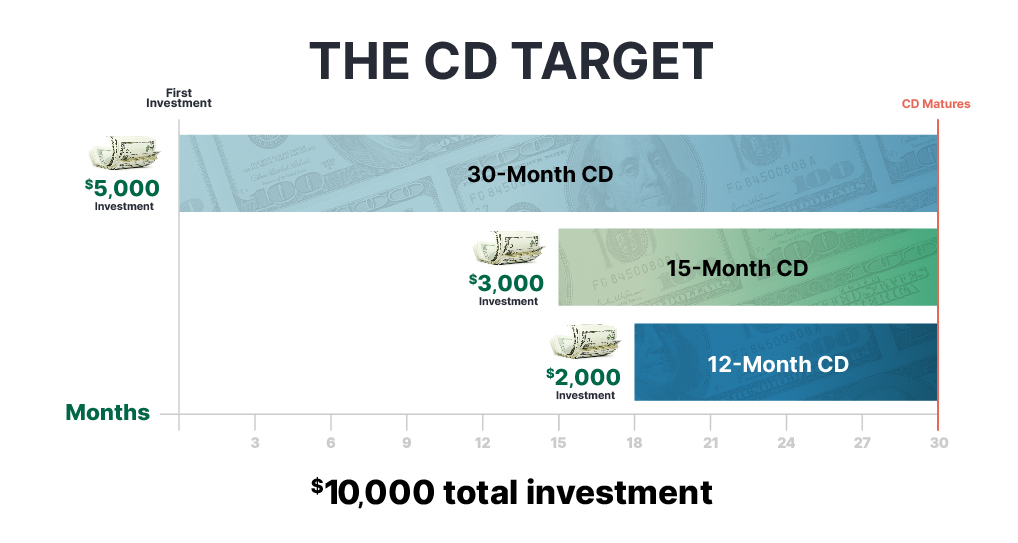

The CD Target

With a CD target, you invest in multiple CDs at different intervals, so they all mature around the same time. This strategy allows you to see if rates go up before you invest all your money or invest more as you continue to save. A CD target could also help you save towards a specific goal, like a down payment on a home, or a wedding.

For example, you could:

- Start with $5,000 in a 30-month CD.

- One year later, invest $3,000 in an 18-month CD.

- Six months later, invest $2,000 in a 12-month CD.

Thirty months after you open your first CD, all three CDs mature at the same time. Now, you access to $10,000 plus the interest you earned.

This gives you an opportunity to build your earnings, but also leaves flexibility to keep money if you end up needing it.

Learn more: CD Target Strategy

When a CD Isn’t Right for You

As simple as CDs are, they are not always the best choice for growing your savings. Here are a few situations where a CD may not be your best option:

- You want immediate access to your funds.

- You’re okay with a higher risk profile.

- You think CD rates may go up soon.

- You find better rates from high-yield savings accounts or money markets.

Frequently Asked Questions About CDs

- Renew your CD at its rate at that time.

- Roll it into a different CD with a different term and/or rate.

- Withdraw the funds and earnings and close your CD without penalty.

Choose a Strategy That Works For You

Investing your money in a CD is a simple way to grow your savings. But a little creativity can help you add flexibility while keeping your earning potential high.

If you’re ready to start exploring your options, we have a variety of CD terms with great rates to fit your savings approach.