How a Home Equity Line of Credit (HELOC) Can Help You Achieve Financial Freedom

Achieve your dream of financial freedom.

Published Thursday, January 9, 2025 to Advice

The information below is for educational purposes only.

Let’s talk about the things you pay for.

First, you have your bills for things like credit cards, student loans, medical expenses and more. Then there are the things you’re looking forward to like home renovations, going back to school for a master’s degree, or starting a business. The list could go on and on.

Whether you’re focusing on getting out of debt, or making other improvements to your life, the answer could be the same: a home equity line of credit (HELOC).

Let’s dive into how HELOC rates can help you achieve financial freedom. But first, let's talk about what a HELOC is and how it's different from a closed-end home equity loan.

What is a Home Equity Loan

A home equity loan allows you borrow against the equity in your home. To determine your equity, you subtract the amount you currently owe on your mortgage from the value of your home.

So, if your home’s value is $350,000 and your current mortgage balance is $250,000, you have $100,000 in equity. That means you could borrow $100,000 with a home equity loan.

With closed-end home equity loans, you borrow a pre-determined amount up front and pay it back on a set schedule. A closed-end home equity loan is perfect for big expenses for which you know the total costs and need the lump sum all at once.

What is a Home Equity Line of Credit (HELOC)?

A HELOC is a different type of home equity loan. Just like with a closed-end home equity loan, you use the equity in your home to determine the amount you are eligible for.

Unlike a closed-end home equity loan, a HELOC is an open line of credit. This means you can use it repeatedly as needed. It's perfect for expenses where you don't know the full cost up front, or want to pay as you go.

Veridian offers closed-end home equity loans and HELOCs, so you can meet your financial goals your way.

Below, we'll talk about the different things you can use a home equity loan or a HELOC for.

Just the facts: What are the benefits of a HELOC

A Home Equity Line of Credit is a flexible funding source.

Get the factsUnderstanding Veridian's HELOC Options

At Veridian, you can choose between two types of HELOC:

- Fixed-Rate HELOC: Fixed interest rate for the first five or 10 years, then variable.

- Variable-rate HELOC: Your rate adjusts with market conditions.

How Do Home Equity Line of Credit Rates Work?

Usually, HELOC rates are variable for the entire term of the loan. This means your rate may change from time to time, depending on market conditions.

Some lenders, however, offer fixed rates for a certain amount of time. In these situations, you can rest easy knowing that your rate won’t fluctuate for the first five or 10 years.

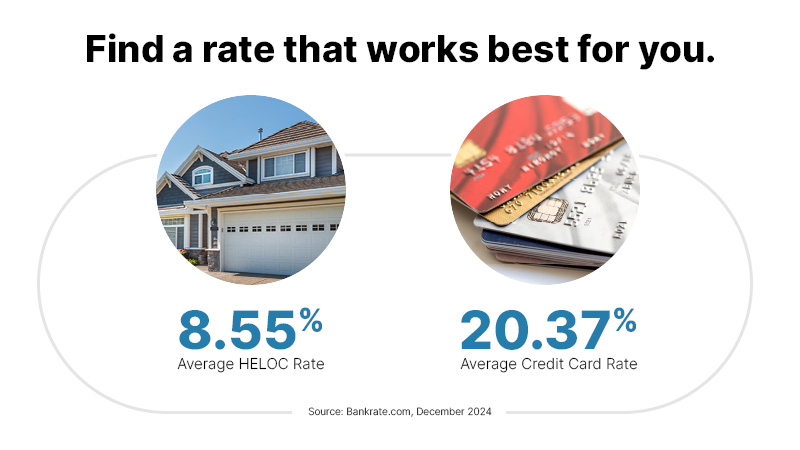

Plus, HELOC rates are usually lower than other types of debt like credit cards, student loans and more. This makes it a good option for a wide variety of uses.

Using a Home Equity Line of Credit to Get Out of Debt Faster

Since HELOC rates are lower than other types of credit, they can be used to help you get out of debt faster.

Pay Off High-Interest Credit Cards

If you have a large balance on a high-interest credit card, you may refinance it in a HELOC. According to The Mortgage Reports, credit card rates tend to be 10% – 15% higher than HELOCs. You’ll pay less interest over time and may be able to pay it off sooner.

Refinance Student Loans

If you have private student loans with high interest rates, refinancing them into a home equity line of credit could simplify payments and reduce your costs.

Cover Medical Expenses

You can use your HELOC to pay for required or elective medical expenses. This could include things like infertility treatments, cosmetic surgeries and more.

Other Debt Refinancing Options

A home equity line of credit is versatile and can be used to refinance various types of debt, helping you save money and streamline payments.

Using a Home Equity Line of Credit to Improve Your Life

HELOC rates aren’t just good for getting out of debt. You can also use them to improve your life. Let’s look at some examples.

Make Home Improvements

Are you ready to finally have that dream kitchen? Or that home office? How about that gorgeous outdoor living space?

No matter what home improvements you’re considering, a HELOC can help you pay for it. Most likely with a lower interest rate than a credit card.

Fund Education

Whether you’re sending your kids off to college for the first time or you’re ready to go after your master’s degree, you can finance an education with a HELOC. In many cases, you may save money over a traditional student loan.

Start a Business

If you’re an aspiring business owner, you’ve probably heard the phrase “you have to spend money to make money.” Well, you can get your startup money by using a HELOC.

Key Factors When Considering a Home Equity Line of Credit

When exploring HELOC options, it’s important to compare features carefully. Here’s why Veridian stands out:

- Flexible Rates: Choose between variable and fixed-rate options.

- Equity Requirements: Borrow based on the value of your home and remaining mortgage balance.

- Competitive Offers: Take advantage of promotional rates and fee reductions.

When a Home Equity Line of Credit May Not Be the Best Option

A HELOC isn’t always going to be the best solution to achieve your financial goals. Here are a few instances where you won’t want to use a HELOC:

- Other loan options have a better rate or term.

- You don’t have enough equity in your home.

- You don’t want to borrow against your home’s equity.

How to Apply for a Home Equity Line of Credit

The requirements for getting a HELOC are like other types of loans. Your credit score and history will play a big role. For a HELOC, you also need to own your home and have equity in it.

You don’t need to own your home outright. You may have a mortgage on your home and get a HELOC. However, most financial institutions will need to be in the first or second lien position for you to qualify.

When you apply for a HELOC here is a short list of the documents and information you will need on hand:

- Documentation of household income

- Your Social Security number

- A recent mortgage statement

- A property tax bill

- A copy of your homeowner's insurance policy

These requirements may vary depending on your lender. Check with them before you apply.

With most lenders, you can start your application online or schedule an appointment with an expert for more advice.

Frequently Asked Questions About Home Equity Lines of Credit

Take Advantage of Competitive HELOC Rates Today

At Veridian Credit Union, we have a full range of home equity loan products, including closed-end loans and HELOCs. Our rates are great, and we have special offers and intro rates throughout the year.

Let us help you achieve financial freedom. Click below to learn more about our HELOC options and apply today.

I want more information Show me HELOC rates Schedule an appointment